Average Personal Injury Settlements in Texas: Understanding What Your Claim is Really Worth (2026)

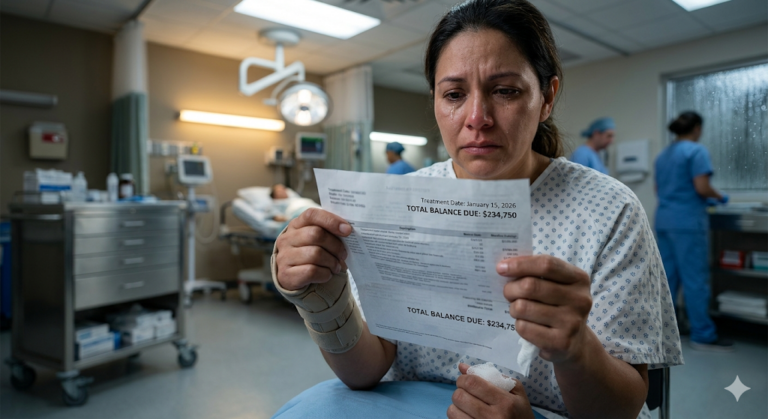

When someone is injured, one of their initial concerns is about the amount of compensation they will receive. Despite the enticing advertisements claiming significant payouts for injuries, individuals are more interested in practical answers rather than marketing hype. They seek reassurance that any settlement they receive will be adequate to cover their expenses and provide for their family’s future.

In the year 2026, there is no set average for personal injury settlements in Texas. Each case is unique, tailored to the individual circumstances of the victim. For instance, a broken leg for a professional athlete may hold more legal weight compared to the same injury sustained by a retired person. This distinction is due to Texas laws aiming to restore the victim to their pre-injury state. This article will delve into the fundamental aspects of a settlement, contrasting the “multiplier” and “per diem” approaches, and will uncover five hidden factors that could significantly increase the value of your claim. Ultimately, the focus should be on determining the maximum value of your specific losses, as opposed to fixating on an average figure.

The Two Pillars of Settlement Value: Economic and Non-Economic Damages

To assess the worth of your case, you need to categorize your losses into two groups. The first category is Economic Damages, which consist of quantifiable expenses such as medical bills, medication costs, and lost wages following the incident. Additionally, future expenses like surgeries and therapy are also considered.

The second category, often more significant, is Non-Economic Damages. This area encompasses intangible losses like Pain and Suffering, emotional distress, physical changes, and the impact on your quality of life. While it’s challenging to assign a monetary value to emotional distress, insurance companies might attempt to diminish the importance of this aspect of your claim. Essentially, while economic damages set a minimum for your settlement, non-economic damages establish the maximum compensation you may receive.

What goes into the valuation:

- Past and Future Medical Bills: From the ambulance ride to your 20th therapy session.

- Lost Wages: Not just the time you missed, but the promotions and bonuses you lost.

- Loss of Earning Capacity: If you can no longer do the job you were trained for.

- Physical Impairment: Compensation for being unable to walk, run, or lift your children.

Practical Tip: Keep a “Pain Journal.” Documenting how your injury affects your daily life (e.g., “Could not attend son’s soccer game due to back pain”) provides the concrete examples needed to push your non-economic damages to the maximum limit.

The Multiplier Method: How Lawyers and Adjusters Do the Math

In negotiations held in 2026, both parties typically employ a strategy to establish a starting point. One common approach is the Multiplier Method, where your overall economic losses (e.g., $50,000 in medical expenses) are multiplied by a factor ranging from 1.5 to 5.

A lower multiplier (1.5) is utilized for minor, temporary injuries with full recovery, while a higher multiplier (4 or 5) is applied for permanent disabilities, scarring, or traumatic brain injuries. For instance, if your medical costs amount to $100,000 and the multiplier is 4, your total settlement request would be $400,000 for pain and suffering in addition to the $100,000 for expenses, totaling $500,000. Ultimately, your attorney’s role is to advocate for the highest feasible multiplier by demonstrating the seriousness of your injuries.

Factors that increase the multiplier:

- Severity of the Injury: A fractured skull is worth more than a bruised rib.

- Clarity of Fault: If the other driver was 100% responsible (e.g., drunk driving).

- Impact on Lifestyle: If you can no longer participate in hobbies you once loved.

- Length of Recovery: Cases involving 12+ months of treatment command higher values.

Warning: Insurance companies use AI software to calculate these numbers. If you don’t have a human advocate to point out the “human” details the software misses, you will almost certainly get a lowball offer.

Estimated Settlement Ranges by Injury Type (Texas 2026)

| Injury Type | Typical Severity | Estimated Settlement Range | Key Driver of Value |

| Soft Tissue / Whiplash | Minor to Moderate | $15,000 – $45,000 | Consistency of medical treatment. |

| Simple Bone Fracture | Moderate | $50,000 – $150,000 | Impact on work and mobility. |

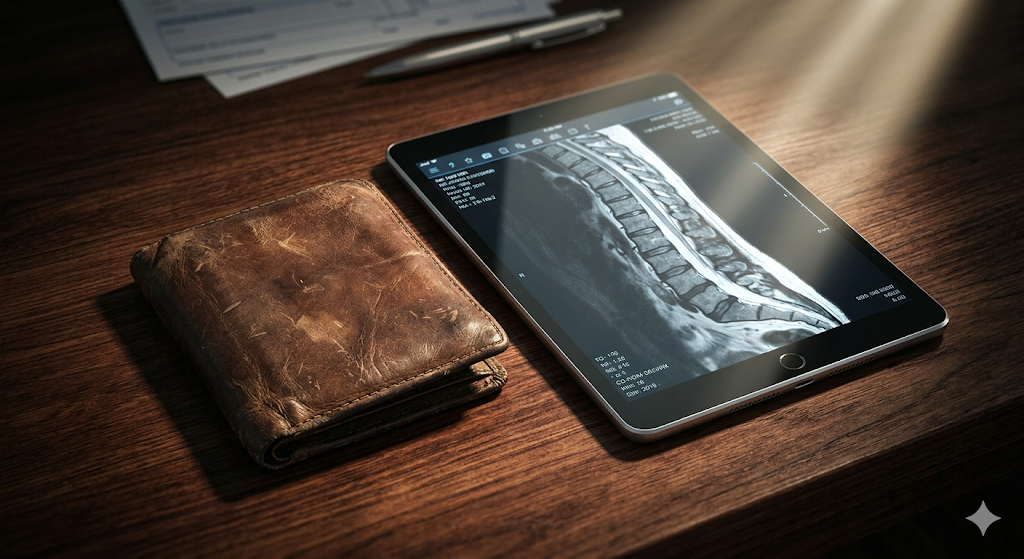

| Spinal / Herniated Disc | Severe | $150,000 – $500,000+ | Need for future surgery or injections. |

| Traumatic Brain (TBI) | Catastrophic | $500,000 – $5,000,000+ | Life Care Plan and long-term care needs. |

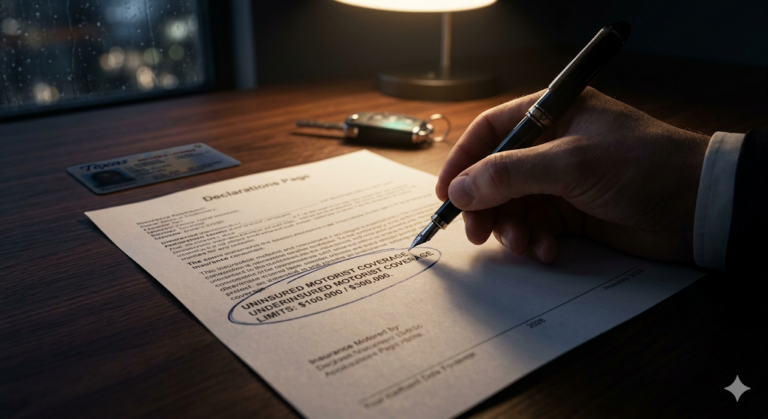

Hidden Factors: Insurance Limits and Policy “Stacking”

It is possible to have a case that is valued at $1,000,000, but if the individual who caused the accident only carries the minimum insurance coverage required in Texas, which is $30,000, it can pose a problem. The amount you can receive in a settlement is frequently restricted by the available insurance coverage. This is why we explore the option of having Multiple Insurance Policies.

In 2026, we will examine whether the driver was on the job during the accident (which could trigger a business policy), if they were driving a vehicle belonging to someone else, or if you have Uninsured/Underinsured Motorist (UM/UIM) coverage within your own policy. At times, we can combine these coverages to guarantee that you receive the complete compensation for your claim, even if the at-fault driver lacks financial resources. Ultimately, the maximum amount you can recover in your case is determined by the origin of the funds.

How we find extra money for your claim:

- Corporate Liability: Suing the employer of a distracted driver.

- Umbrella Policies: Accessing high-value secondary insurance for wealthy defendants.

- Product Liability: Suing the car manufacturer if a defect (like an airbag failure) made the injury worse.

In my experience, the difference between a $30,000 check and a $300,000 check is often the lawyer’s ability to find every available insurance policy.

Common Legal Questions Regarding Settlement Values

How long will it take to get my settlement check?

Most personal injury cases in Texas typically require 6 to 18 months to be resolved. Rushing to settle prematurely could result in overlooking latent injuries that may surface later. Our approach involves waiting until you have reached Maximum Medical Improvement (MMI), a stage where your medical providers can accurately predict your future condition, before initiating substantial discussions. Settling prior to reaching MMI is identified as the primary reason for financial losses in a claim.

Does my settlement include money for taxes?

Typically, settlements related to physical injuries and the resulting emotional distress are not taxable according to IRS regulations. However, any part of the settlement designated as “Punitive Damages” or “Interest” might be taxable. It is advisable to seek advice from a tax expert to safeguard your final settlement amount.

Will my previous injuries lower my settlement value?

The insurance provider may attempt to argue that your existing pain is simply a “pre-existing condition.” Nevertheless, according to the “Eggshell Skull Rule,” a defendant is accountable for all the damage they caused, regardless of your higher susceptibility. If the accident exacerbated a prior injury, you are still eligible for compensation for the worsening of that condition.

Conclusion

An average settlement is merely a number, while your compensation is crucial to your well-being. By grasping the importance of both financial and emotional losses, employing the multiplier approach, and exploring all potential insurance coverage, you can surpass ordinary outcomes and obtain the highest possible compensation that you are entitled to. You may not have chosen to be injured, but you have the power to ensure that those at fault are held responsible for reimbursing you for all your damages.

Key Takeaways:

- Value is Personalized: Your career and lifestyle dictate the final number.

- Multiplier Matters: Proving the severity of pain is the key to a larger check.

- Don’t Settle Early: Wait for MMI to ensure all future costs are covered.

- Check the Limits: Your settlement is often tied to the insurance policies available.

Concentrate on your physical therapy and recovery process. Leave the intricate calculations and discussions with the insurance companies to the legal experts. You deserve complete compensation for your losses, and in 2026, the law supports your cause.

IMPORTANT LEGAL DISCLAIMER: This article is intended for educational purposes and information only, and should not be considered as legal counsel. Regulations differ depending on the state and area. Each accident and injury lawsuit is distinct. If you have been hurt, it is advisable to seek guidance from a competent personal injury lawyer in your locality for tailored advice.