Uninsured and Underinsured Motorist (UM/UIM) Claims: How to Get Paid When the Other Driver Has No Money (2026)

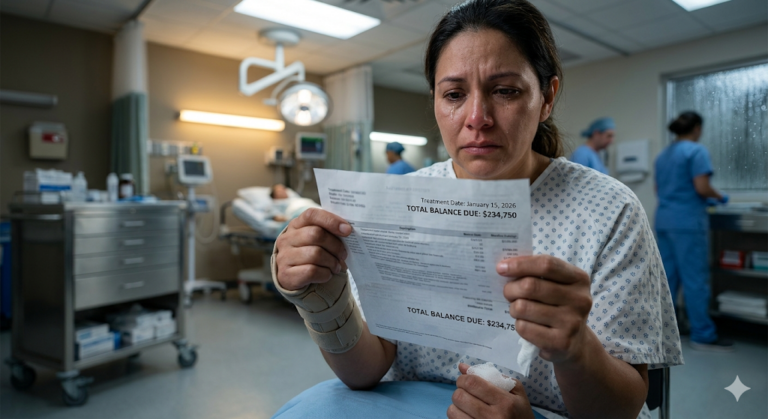

You have experienced a severe accident where your car is completely damaged, and you need surgery for your injuries. Initially, you hoped that the other driver’s insurance would cover all expenses, but then you discover that the driver is uninsured or only has the minimum coverage, which is insufficient for your medical bills. This situation leads to worry and uncertainty about how to manage the financial burden caused by someone else’s negligence.

In 2026, dealing with Uninsured (UM) and Underinsured Motorist (UIM) claims in Texas is a complex legal process with high stakes. Many individuals are unaware that they have a backup plan in their own insurance policy. Nevertheless, it is crucial to understand that when you file a UM/UIM claim, your own insurance provider, whom you have been paying for years, can turn into your legal adversary. They may attempt to diminish the value of your claim just like the other party’s insurer. This article will detail the steps to activate your UM/UIM coverage, strategies to combat “Insurance Bad Faith,” and why your own policy could be your most valuable resource in recovering from a 2026 accident.

The Difference Between UM and UIM: Knowing Your Coverage

In Texas, insurance companies must provide UM/UIM coverage by law unless you decline it in writing. Uninsured Motorist (UM) coverage becomes effective when you are in an accident caused by a driver without any insurance or in a hit-and-run situation where the driver flees. Underinsured Motorist (UIM) coverage comes into play when the other driver is insured but their policy doesn’t cover all your damages due to insufficient limits.

Based on my observations, UIM claims are the most frequent in 2026. For instance, if your medical expenses amount to $100,000 and the at-fault driver’s insurance only covers $30,000, your UIM policy would pay the remaining $70,000 (up to your policy limits). Essentially, these coverages are intended to bridge the gap and guarantee that your physical recovery is not hindered by someone else’s poor financial decisions.

Why UM/UIM is vital in 2026:

- Hit-and-Run Protection: It is the only way to get paid if the driver disappears.

- Catastrophic Injury Security: High-value injuries almost always exceed the Texas state minimum.

- Legal Leverage: It forces your insurer to step into the shoes of the negligent driver.

- Stacking Protection: It provides an extra layer of financial security beyond the at-fault driver’s assets.

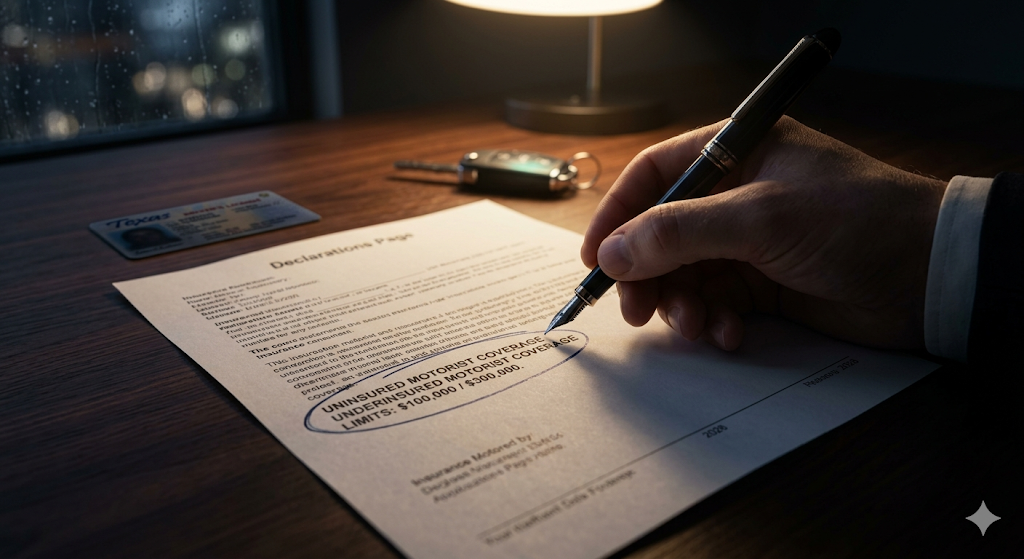

Practical Tip: Check your “Declarations Page” today. If you see “UM/UIM” with limits of $100,000/$300,000 or higher, you are in a much stronger position. If you don’t see it, you may have unknowingly signed a waiver.

Why Your Own Insurance Company Becomes Your Enemy

Dealing with the legal process can be highly frustrating, especially when you anticipate your insurance company to support you. However, in an UM/UIM claim, the focus of the company shifts towards reducing their payout. They may resort to typical tactics used by insurers such as arguing that your injuries existed prior, attributing partial fault to you, and proposing a meager settlement to test your desperation.

From my own experience, succeeding in a UM/UIM claim requires treating it as a full-fledged lawsuit. It is essential to establish the negligence of the other driver and demonstrate the complete extent of your losses. The crucial point is that you are not just a “customer” anymore; you are now a “claimant.” A well-thought-out strategy is necessary to compel them to fulfill the terms of the contract you have been contributing to.

Tactics insurers use to deny UM/UIM claims:

- Challenging Liability: Claiming the uninsured driver wasn’t 100% at fault.

- Devaluing Medical Care: Saying your treatments were “excessive” or “not necessary.”

- Delaying the Process: Hoping you will get frustrated and accept a smaller check.

- The “Consent to Settle” Trap: If you settle with the at-fault driver without your insurer’s permission, you might lose your right to UIM benefits.

UM/UIM vs. Standard Liability Claims: Key Differences

| Feature | Standard Liability Claim | UM/UIM Insurance Claim |

| Defendant | The At-Fault Driver’s Insurer. | Your Own Insurance Company. |

| Basis of Claim | Negligence of the other driver. | Contract Law + Negligence. |

| Primary Hurdle | Proving fault. | Proving damages exceed the other policy. |

| Recovery Limit | The other driver’s policy max. | Your own policy max. |

Proving “Underinsurance”: The Math of Your Settlement

In Texas, in order to succeed in a UIM claim, it is necessary to demonstrate that the insurance of the responsible driver has been fully utilized, which is referred to as being “exhausted.” This implies that the entirety of their policy limit has been disbursed to you, allowing you to then tap into your UIM coverage. For instance, if you have a lasting spinal injury valued at $500,000, and the other driver is insured for $50,000, the initial step is to recover that $50,000.

It’s crucial to accurately determine the value of your case rather than making assumptions. To establish that your future medical expenses will exceed the coverage provided by the other driver’s insurance, we rely on Medical Experts and Life Care Planners. Essentially, a UIM claim centers on identifying “the gap.” Without concrete evidence of this gap, your insurance provider will not make any payments.

Evidence needed for a UIM claim:

- Exhaustion Letter: Proof that the other driver’s insurer paid their full limit.

- Expert Valuations: Proving your “Pain and Suffering” and “Lost Wages” are high-value.

- Policy Documents: Your original insurance contract showing your coverage levels.

Warning: Always get “Written Consent” from your insurance company before you sign any release with the at-fault driver. If you don’t, your insurer may claim you “prejudiced their subrogation rights” and deny your UIM claim entirely.

Common Legal Questions Regarding UM/UIM Recovery

Will my insurance rates go up if I file a UM/UIM claim in Texas?

According to Texas regulations, in most cases, an insurance provider is not allowed to raise your rates due to an accident that was not caused by you. As uninsured/underinsured motorist claims are related to the responsibility of the other driver, you should not face a penalty for utilizing the insurance you have been paying for. If your insurance company attempts to hike your premiums, they could be breaking the rules outlined in the Texas Insurance Code.

What if I was a passenger in someone else’s car?

If you were riding as a passenger, you might have coverage under both the driver’s UM/UIM policy and your own UM/UIM policy. This practice is referred to as “stacking” in specific situations (although Texas has particular guidelines on its application). From my observations, we thoroughly review all policies within the household to guarantee that you have access to the maximum available funds for your rehabilitation.

Is there a time limit for filing a UM/UIM claim?

Certainly! However, it varies from a typical car accident as a UM/UIM claim is considered a Contract Dispute. In Texas, the statute of limitations is generally four years from the date the insurance company violated the contract, which typically occurs when they reject your claim. Nonetheless, it is advisable not to delay that long. You must still demonstrate that the initial accident occurred within the two-year personal injury timeframe. Taking prompt action is crucial to safeguarding evidence.

Conclusion

Discovering that the individual who caused the accident does not possess insurance can be a distressing situation. However, this does not signify the conclusion of your journey towards recuperation. In the legal environment of Texas in 2026, your UM/UIM policy stands out as the most crucial decision you have ever taken. By grasping the Exhaustion procedure and ensuring that your insurance provider adheres to their agreement, you can obtain the necessary funds to fully recover. Do not allow the error of an uninsured driver to shape your financial prospects.

Key Takeaways:

- Fill the Gap: Use UIM when the other driver’s policy is too small for your injuries.

- Treat it Like a Lawsuit: Your insurer is your opponent in a UM/UIM claim.

- Get Consent: Never settle with the other driver without your insurer’s written permission.

- You Paid for It: Don’t be afraid of rate hikes; you have a legal right to this coverage.

Concentrate on your physical recovery and your loved ones. Leave the legal experts to deal with the fight against the large insurance companies. You deserve the coverage you have invested in and you deserve fairness, regardless of who caused the accident.

IMPORTANT LEGAL DISCLAIMER: This article is intended for educational and informational purposes exclusively and should not be considered as legal counsel. Legal regulations differ depending on the state and area. Each accident and injury lawsuit is distinct. If you have sustained an injury, it is advisable to seek guidance from a competent personal injury lawyer in your vicinity tailored to your circumstances.