Car Accidents in Texas: How to Maximize Your Compensation in 2026

You’re driving through a assiduous crossroad in Dallas or Houston, allowing about your coming gathering. Abruptly, the world spins. The sound of scraping essence and bursting glass fills the air. You’ve been smash. As the dust settles, the physical pain thresholds, but the internal pressure is indeed worse. How will you pay for your auto? Who’s going to cover these mounting ER bills? Most importantly, how do you deal with an insurance company that’s formerly trying to condemn you for the crash?

In the fate of a Texas auto accident, you are not precisely a motorist; you’re a” descendant ” in a high- claims legit battle. The opinions you make in the first 48 hours can determine whether you admit a$ 5,000 agreement or a$ 500,000 payout. This composition will draw ago the cope on the legit

process. You will get how Texas fault ordinances work, what damages you can really assert, and how to cover your birthrights from ambitious adjusters. The nethermost line is that you earn a agreement that covers your future, not precisely your history.

Understanding Texas “At-Fault” and Comparative Negligence Laws

Texas is an” at- fault” country. This means the person who caused the accident is responsible for the damages. still, Texas also uses a rule called Modified relative Negligence( specially the 51 Bar Rule). This is a favorite device for insurance companies. They will try to establish you were at least incompletely responsible for the crash to reduce the quantum they’ve to pay you.

For illustration, if a jury decides you were 20 at fault because you were hardly speeding, your final agreement check will be downgraded by 20. But then’s the thing if they can establish you were 51 or further at fault, you get nobody. Not a single cent. In my experience, adjusters exercise recorded statements to trick you into fessing fault. They want to shove your chance above that 51 line to close the case for free.

Here’s what you need to know about fault in Texas:

- Duty of Care: Every driver has a legal duty to follow traffic laws and stay alert.

- Proving Breach: You must show the other driver breached that duty (e.g., texting, running a red light).

- Proximate Cause: You must prove their breach was the direct cause of your specific injuries.

Practical Tip: Never apologize at the scene of the accident. A simple “I’m sorry” can be used as a “confession of negligence” in a Texas court.

Dealing with Insurance Adjusters and Early Settlement Offers

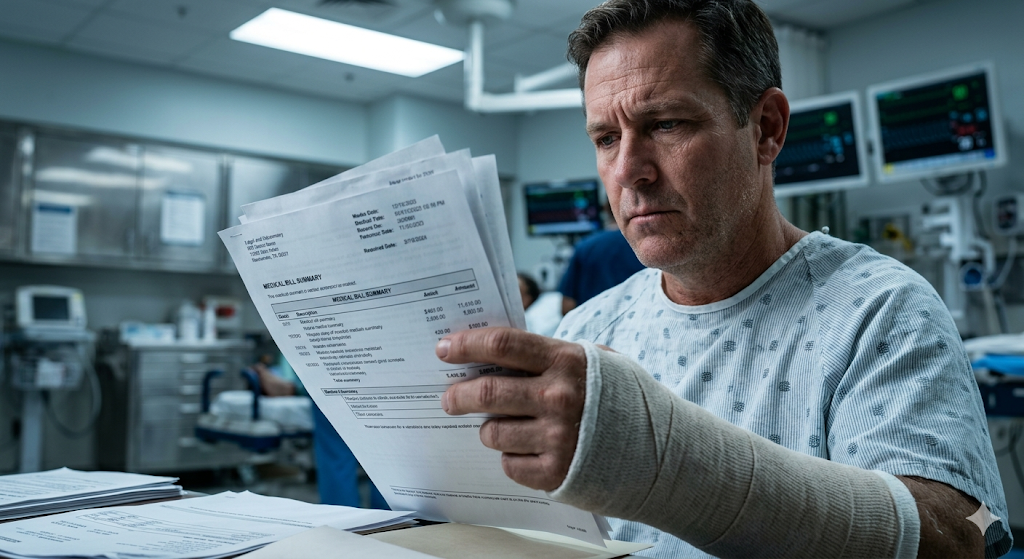

Within days of your accident, you’ll probably admit a cry from the other motorist’s insurance company. The adjuster will sound friendly and humane. They might indeed extend you a check for$ 2,000 or$ 5,000 right down to” help with the bills.” Then’s the thing this is a trap. This is what we call a” gadfly agreement.”

Insurance companies see that your medical bills in 2026 are astronomical.However, your case is through, If you accept that fragile check and subscribe their release shape. Indeed if you detect out coming month that you need a$ 50,000 spinal surgery, you can not interrogate for further plutocrat. The nethermost line is that their thing is to resolve the claim for the smallest quantum practicable before you realize how hurt you truly are.

Common adjuster tactics include:

- Requesting a Recorded Statement: They want to catch you in a contradiction.

- Delaying the Claim: They wait until your bills go to collections so you get desperate.

- Requesting a Total Medical Release: They want to dig through your records from 10 years ago to claim your injury was “pre-existing.”

Warning: You are not legally required to give a recorded statement to the other driver’s insurance company. Ever.

Car Accident Settlements: What’s Actually Covered?

| Damage Category | What is Included? | Why You Need an Attorney |

| Economic Damages | Medical bills, ER visits, surgery, lost wages. | To ensure future medical costs are accurately calculated. |

| Non-Economic Damages | Pain and suffering, emotional distress, scarring. | To translate your “human suffering” into a dollar amount. |

| Property Damage | Car repairs or the “Fair Market Value” if totaled. | To fight for the actual replacement cost, not a lowball value. |

The Importance of PIP and UM/UIM Coverage in Texas

In my experience, numerous fatalities are shocked to detect out the person who smash them has” minimal limitations” insurance. In Texas, the minimal incommodity for fleshly injury is$ 30,000 per person.However, 000, that$ 30, If your sanitarium bill is$ 100. This is where your own procedure becomes your lifesaver through particular Injury Protection( PIP) and Uninsured/ Underinsured Automobilist( UM/ UIM) content.

PIP pays for your medical bills and a portion of your lost stipend anyhow of who caused the crash. UM/ UIM kicks in when the at- fault motorist either has no insurance or does not have enough to cover your grand damages. Under Texas law, your insurance company must extend you these contents in writing.However, and you do not have them, you may still be suitable to assert them, If they did n’t.

Benefits of these coverages:

- No-Fault Benefits: PIP pays even if the accident was partially your fault.

- Gap Filling: UM/UIM covers the difference between the other driver’s limit and your actual loss.

- Peace of Mind: It protects you from the thousands of uninsured drivers on Texas roads.

Practical Tip: Check your “Insurance Declarations Page” today. If you don’t see UM/UIM, call your agent and add it immediately. It is the cheapest way to protect your family.

Why the 2-Year Statute of Limitations is a Hard Deadline

Time is the adversary of your auto accident claim. In Texas, the Statute of terminations for particular injury cases is usually two times from the assignation of the crash. You might suppose two times is a long time, but it moves presto when you’re concentrated on surgeries and physical remedy.

still, your birthright to indemnification vanishes ever, If you do not file a conventional action in a Texas court before that alternate anniversary. No expostulations. In my experience, insurance companies will” negotiate” with you for 23 months, making you suppose they will pay. Once the 24th month passes, they will stop returning your calls because they see you can noway longer sue them.

Things that disappear over time:

- Evidence: Skid marks fade, and cars are crushed and recycled.

- Witnesses: People move, change phone numbers, and forget details.

- Video Footage: Most gas stations and traffic cameras overwrite their data every 7 to 30 days.

The bottom line is… you should treat the first 30 days after an accident as the “Golden Hour” for evidence collection.

Frequently Asked Questions (FAQ)

1. How much is my Texas car accident case worth?

There’s no” magic calculator.” agreement valuations hinge on the inflexibility of your injuries, the quantum of insurance content accessible, and the clarity of the substantiation against the other motorist. Cases can categorize from$ 15,000 to through$.

2. What is a “Letter of Protection” (LOP)?

An LOP is a legit document transferred by your attorney to a croaker . It allows you to get medical treatment now without paying outspoken. The croaker agrees to stay for payment until your case settles. This is vital for fatalities who do not have health insurance.

3. Should I go to the doctor if I don’t feel “that bad”?

Yes. Adrenaline frequently masks serious injuries like internal bleeding or concussions.However, the insurance company will argue that you were not really hurt or that commodity differently caused your pain, If you stay a week to know a croaker .

Conclusion

A auto accident in Texas is further than precisely a concussion of instruments; it’s a concussion of interests. You want to get healthy and pay your bills. The insurance company wants to cover its nethermost line. By gathering the regulations of relative Negligence and the exact Statute of terminations, you set yourself in a situation of authority. Do not allow an adjuster’s friendly tone fool you they are trained to minimize your loss.

Key Takeaways:

- Preserve the Percentage: Don’t admit fault; let the evidence speak.

- Reject Early Offers: Your “nuisance” settlement will likely be far too low.

- Check Your Policy: Use your PIP and UM/UIM coverages to fill the gaps.

- Watch the Clock: Two years is the limit, but the first 30 days are the most critical.

Focus on your recovery and getting back on your feet. When you have the right information and a professional on your side, the legal system can work for you, not against you.

IMPORTANT LEGAL DISCLAIMER: This composition is handed for instructional and instructional purposes only and doesn’t constitute legit guidance. ordinances vary by country and governance. Every accident and injury case is unique.However, please confer with a good particular injury attorney in your area for guidance special to your situation, If you’ve been injured.